The online mortgage brokerage space continues to adapt as the key players evolve their client experience and funding partners. Attempts vary between single super brokers with assistants (licensed or unlicensed), salaried mortgage agents with volume bonuses and retail storefronts mimicking the traditional bank model or a mixture thereof. As funding volumes or invested capital permits, these online brokerages then pursue their own monoline or exclusive white label funding partners. Ultimately, by taking full control of the complete mortgage origination cycle, they maximize their overall basis point income. Their advantage is rate and systems.

impact on various brokerages

Independent mortgage brokers, meanwhile, have the distinct advantage of being nimble and able to adjust quickly. They have the ability to adopt the most cutting-edge innovations whilst utilizing various readily available tools, without the restrictions of a network’s speed to adapt. Depending on an independent office volume, some may experience restricted lender options and overall lack of resources and support. However, like any business, the entrepreneurial and creative brokers will thrive and overcome any obstacles that may present themselves to an independent broker. Their advantage is relationship, specialization and knowledge.

Franchise or network member brokerages, however, are at the biggest crossroads—or perhaps facing the greatest opportunity to innovate, given their agent numbers. Such brokerages pay fees for which they expect brand equity, marketing, administration and innovative technology of which they couldn’t avail themselves. As these brands are evolving from the traditional percentage split to a flat fee structure, they will be forced to recuperate the lost revenue from other points in the mortgage origination process. Hence, the major brands are quickly developing or acquiring fintech platforms that will enhance the overall client experience, whilst ensuring data and basis point revenue control. Their advantage is the same as that of independent brokers, albeit with some brand equity and access to additional resources.

innovation to come

The mortgage industry’s fintech is evolving at an unprecedented pace and valuation, from the basics such as auto-population of application form data and the ability to pull bank statements and income tax records to automatic document collection and the electronic signing of mortgage documents. With this connection already in place, in the coming months, down payments will be able to be validated automatically. And open banking is coming—the federal government is actively working on open banking draft regulations. This, in turn, will surely lead to automatic CRA income validation, since no financing institution, insurer or government wants to expose itself dealing with mortgage fraud. This type of automatic income validation via banks and governments has already existed in some European countries for years (e.g. Germany), and there’s no reason to believe Canada won’t follow suit.

Meanwhile, property valuation methods are experiencing a rapid evolution of their own. Lenders and insurers are increasing their adoption of automatic valuations models (AVM). Some provincial governments (e.g. Saskatchewan, Manitoba, etc.) have in recent years privatized their land title offices. In Manitoba, the title registrar even operates as “Teranet,” the same company that offers its “PurView” property valuation system to both brokers and lenders alike. As fintech and automatic property valuation models integrate, mortgage origination platforms will become increasingly seamless.

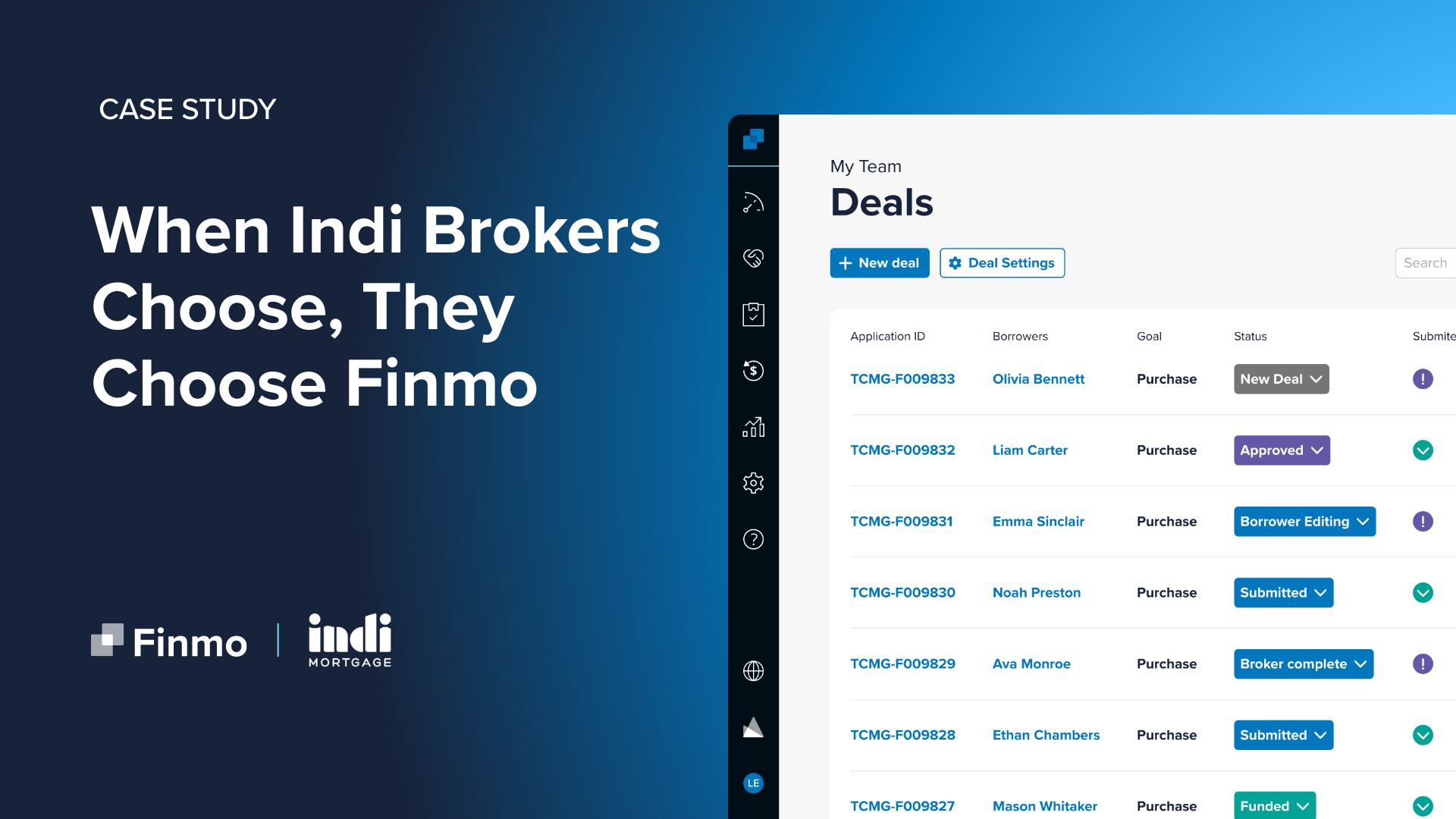

The rise of the digital mortgage origination platform

For years, there was a single mortgage origination platform in Canada (Finastra’s Filogix Expert) that processed the majority of broker-initiated transactions. This was due to its longstanding connection relationship with lenders. Its “link” service allows alternate platforms to utilize its connection channels with lenders for a fee. Three alternate platforms (Finmo, Velocity, and Mortgage Boss) are rapidly growing their market share. Although the Filogix link remains popular with the alternate platforms, they are rapidly developing their own direct submission relationships with lenders in order to capture the compensation paid by lenders to the origination platform provider.

2021 saw the launch of Finmo's Lender Connect, whereby Finmo's application system was directly connected to over 250 lenders. In other words, as fintech evolves at this unprecedented pace, the lenders will have to decide which originated mortgage origination volumes they desire. Since all lenders are driven by their desire to maintain and increase revenue, their cooperation in these direct submission efforts is inevitable.

Regardless of agent, broker, network or platform, though, all mortgages are ultimately originated by the borrower. The borrower is the client, and as a consumer of mortgage or lending products, they dictate the potential of a closed and funded transaction. And just like fintech in the mortgage industry, consumer expectations, demands and even habits are changing at an unprecedented pace.

For a mortgage, a borrower wants to trust a reputable person and/or brand (or default to their trust in their charter bank or credit union from their decades of brand equity). They want the easiest and fastest process with the littlest roadblock (e.g. the ability to take photos of documents to upload via their phone). They want to do it at their own pace, 24/7, whilst communicating in their desired medium (e.g. SMS, chat, video, etc.). Finally, they demand and deserve the best possible mortgage product, ideally from a professional who has their best interest at heart.

Mortgage origination platforms will continue to evolve to meet user demands of the consumer and brokerage channel. Brokerages will evolve, specialize, merge or cease to exist depending on their ability to adjust to the ever-changing landscape, and networks will naturally experience the same. They’ll continue to change their revenue models whilst evolving their brand marketing and value proposition. By adopting and deploying best-in-class technologies, they will enable their agents to provide the highest quality of client service and user experience, thus potentially slowing the direct-to-consumer and direct-to-lender mortgage origination model that fintech will inevitably and rapidly empower. Whomever removes the greatest number of hurdles in the client’s overall journey of obtaining a mortgage will ultimately be best positioned to secure the most business.

If you’re a mortgage broker wanting to assure the long-term viability of your business, your smartest bet would be to investigate all available mortgage origination platforms and choose the one that’s best for your overall client experience.

.png?width=700&name=Email%20Banner%20(4).png)