To increase the chances of getting your application approved with a lender, it's important to be aware of the common reasons for rejection and take proactive steps to avoid them.

We talked to lenders to find out what can cause qualification problems, pre-approval rejections, and declined deals. Here are the things they said are important for a mortgage application:

Importance of credit files

Lenders require recent credit bureau reports; avoid submitting reports older than 30 days. The credit report gives an overview of the applicant's financial history, helping lenders assess their current financial situation for the mortgage application. Even if there's little change in the credit report, adhere to the 30-day time frame to minimize potential issues with the application. Research the minimum credit score required by each lender before submitting the application. Gather information about lenders' credit score requirements before submission to avoid unnecessary delays. If anything is unclear, contact the lender for clarification before investing time in preparing the application.

Importance of Rate Qualification

Utilize the greater of the contract mortgage rate plus 2% or the floor rate set by OSFI (currently at 5.25%) for reliable rate qualification. Following the recommended rate calculation ensures adherence to OSFI rules. Finmo automatically adjusts the qualifying rate based on OSFI rules, making the process straightforward for mortgage brokers.

Importance of Down Payment Confirmation

Provide all necessary paperwork, especially the down payment and income documentation, clearly and promptly to maintain a smooth process with the lender. Ensure accuracy in the provided documentation to avoid potential issues or delays in funding, which could impact interest rates. Be prepared for lenders requesting additional documentation or verification during the application process. A lower down payment leads to a higher loan-to-value ratio, potentially resulting in a less favourable interest rate for the mortgage. Take the time to carefully organize all transactions and paperwork to avoid mistakes that may lead to rejection and wasted time. Follow lenders' guidelines diligently to increase the chances of a successful application and approval.

Importance of Lender Notes

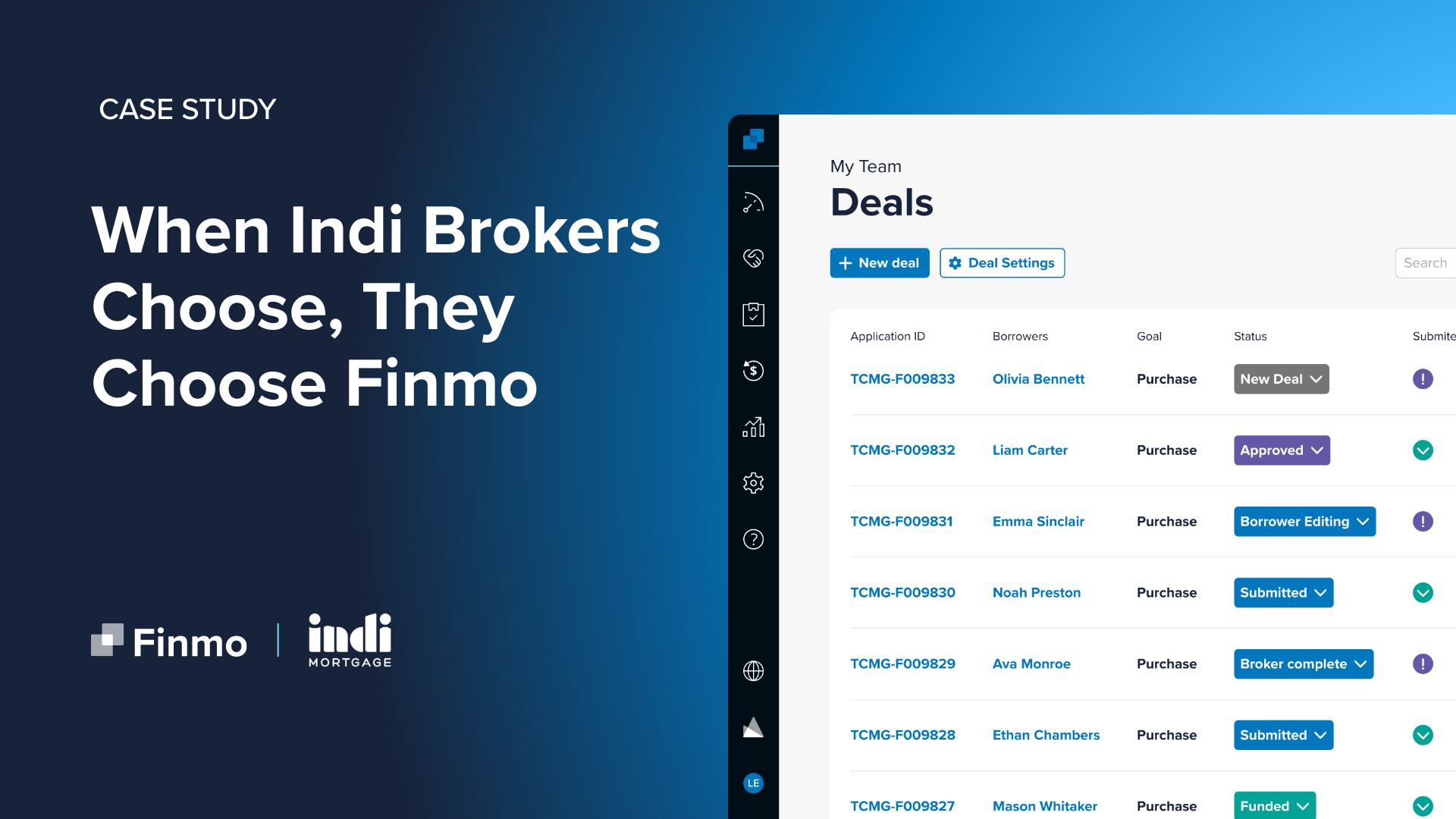

Check the Lender Spotlight section for specific requirements from lenders related to submission tips and underwriting assistance. Use Smart Submission Notes on Finmo to accelerate the packaging note process by up to 75%. Make sure the submission notes have the deal's province, a comprehensive explanation of the case, the preferred term, amortization, the product suitable for the client, details about the financial history, and a walkthrough of the deal itself. Providing more details in the submission notes reduces the underwriter's queries and increases the likelihood of approval.

|

HOT TIP! Want to check if your deal fits with your favourite lenders’ guidelines? Click ‘Find Products’ in Finmo and go to Lender Spotlight to review their policies.

|

Not yet using Finmo or Lender Spotlight? Book a 15 minute discovery call with our team to learn how it can help improve your business.

Already a Finmo client but feel like you need help? Check out our training sessions.